Budget 2026: Navigating the same old challenges

Pakistan’s 2026 budget faces IMF pressure, calls for tax reform, and the tough balance between relief and revenue

Faizan Kamran Khan

Co-Founder, Chief of Strategy & Staff

The author is an entrepreneur and finance professional with a decade of experience in economic research and investment. He is Co-Founder and Chief of Strategy & Staff at Nukta. He is also CEO at FRIM Ventures.

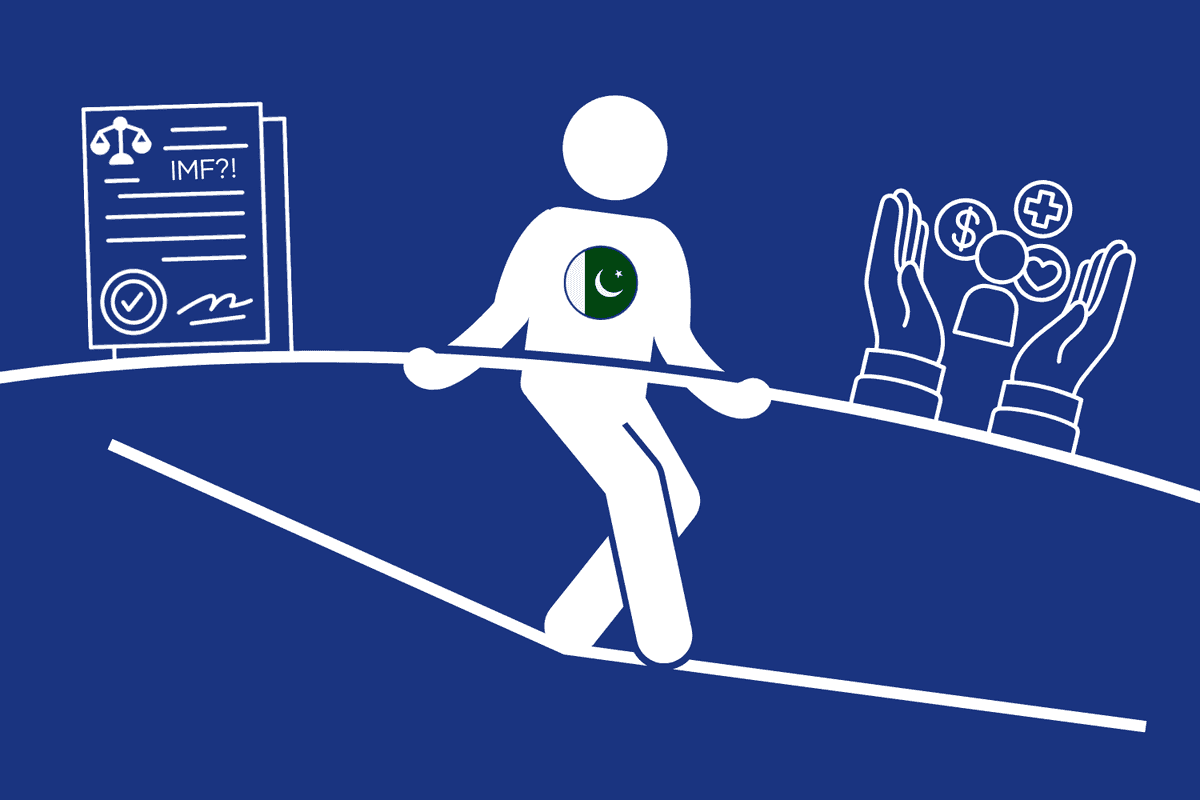

The government is once again caught between a rock and a hard place: fiscal consolidation or much-needed relief?

Nukta

Pakistan’s federal budget is expected to be unveiled on June 10th, and once again, the familiar themes dominate: broadening the tax base, offering relief to the salaried class, and managing fiscal sustainability. Add strict International Monetary Fund (IMF) oversight into the mix, and the government is once again caught between a rock and a hard place: fiscal consolidation or much-needed relief?

Fiscal account: Walking a tightrope

The fiscal deficit remains a major concern. The IMF has emphasized that Pakistan needs to achieve a primary budget surplus of 1.6% of GDP to maintain debt sustainability. Fiscal year 2025 is expected to close at a healthier 2.5% surplus, but that was largely thanks to hefty profits from the State Bank of Pakistan (SBP) — a one-off that won’t repeat next year. With the economy set to move out of stabilization and into growth mode, maintaining the fiscal discipline is likely to be extremely tough.

Tough targets, tougher measures

Unofficial estimates suggest the government is eyeing Federal Board of Revenue (FBR) collections of around PKR 14.3 trillion for fiscal year 2026, up from just under PKR 12 trillion this year. That kind of jump will require more than wishful thinking.

Among the proposals on the table: a 3% sales tax on petroleum products, taxing pension income, withdrawing tax exemptions (such as for the FATA/PATA steel sector), and possibly introducing a “carbon tax” on fuel. But the real game changer — if it can be pulled off — is comprehensively and wholly bringing the massive retail and wholesale sector into the tax net.

Broadening the tax net: A broken record

Calls to expand Pakistan’s tax base are hardly new. The retail and wholesale sectors, despite their size, remain largely untaxed, and untouched. Budget after budget, governments pledge to act, but meaningful reforms remain elusive.

The IMF is pushing hard for change, and rightly so. Arif Habib Limited estimates that taxing these sectors properly could generate PKR 429 billion. If the government can finally execute this long-awaited reform, it could ease the burden on Pakistan’s overtaxed salaried class.

Real estate: Hit where it hurts!

Proposals to stimulate the real estate sector, such as reducing withholding taxes on property transactions and adjusting capital gains tax slabs, are under consideration. The real estate market has remained pretty sluggish over the last couple of years since tax measures were introduced. It seems unlikely that this sector will receive any relief. There are proposals to slash advance taxes to 2% on sale and 1% on purchases compared to 3-4% presently.

But here’s the reality: these tweaks won’t move the needle. The core issue isn’t tax rates, it’s valuation. There’s a massive gap between official FBR values and actual market prices, often up to 50%. Add in widespread cash transactions, and you have a sector that evades taxation almost entirely.

Unless this structural distortion is addressed, meaningful revenue from real estate will remain a pipe dream.

Salaried class: Time for relief?

The salaried class continues to shoulder a disproportionate burden. Tax collections from salaried individuals have skyrocketed — from PKR 76 billion in 2019 to an estimated PKR 570 billion this year. As per Nukta research, in 2024 the salaried class contributed PKR 370 billion in taxation while the retail sector and the agriculture sector contributed a mere PKR 24 billion and PKR 8 billion respectively.

There’s growing pressure to raise the annual exemption threshold from PKR 600,000 to PKR 1 million and revise tax slabs to reflect inflation. A 2.5% reduction in tax rates and adjustments to withholding taxes are under consideration, but all depends on IMF approval, which remains cautious about any relief that could dent revenues.

Debt servicing: Some breathing room

Interest payments on debt have historically consumed a significant portion of Pakistan’s budget. Over the last few years the average for interest payments consuming the country’s total gross revenue is around a massive 50%! Put simply, whatever the government earns in total, half of that goes away in just paying interest on its debt. In fiscal year 2025, interest payments on debt are set to clock in at around PKR 9.1 trillion, or 54% of total budget outlay.

But there’s some good news: with the central bank’s policy rate down to 11% from a high of 22%, the government could save between PKR 500–600 billion in the next fiscal year on interest payments, bringing them down by about 6% in 2026.

Whose budget is it anyway?

Let’s not sugarcoat it: this is an IMF-driven budget. The global lender’s focus on fiscal discipline and structural reform leaves little room for populism or short-term fixes. Every tax tweak and spending line will be scrutinized in Washington and Islamabad.

The government must walk a fine line: aligning with IMF conditions while addressing the political and economic needs at home.

External pressures, lingering woes

Inflation is easing, projected to settle below 5% in fiscal year 2025. But as the economy stabilizes and activity picks up, imports will rise, widening the current account deficit, which the IMF expects to hit around 1% of GDP. Boosting exports and managing import demand will be key. Meanwhile, Pakistan’s external financing needs for fiscal year 2026 stand at a daunting $19.75 billion. A mix of IMF funding, bilateral loans, and multilateral assistance is expected to fill the gap.

Market reaction: Eyes on the tax net

Equity markets will likely take cues from how credible the budget looks in terms of expanding the tax base. With no major changes expected in capital gains or corporate tax rates, the direct impact on stocks should be minimal.

If the government tightens the screws on real estate or other alternative assets, equities might even benefit as capital shifts into the stock market.

Final thoughts

The upcoming budget is yet another test of whether Pakistan can break free from its fiscal Groundhog Day. It must juggle IMF demands, public expectations, and structural realities, all while charting a credible path toward sustainable growth. If the government is serious about reform, this is the time to show it. Half-measures won’t cut it anymore.

*The author is an entrepreneur and finance professional with a decade of experience in economic research and investments. He is Co-Founder and Chief of Strategy & Staff at Nukta. He is also the CEO of FRIM Ventures, a family investment office.

*The views and opinions expressed in this article are those of the author and do not necessarily reflect the editorial stance of Nukta.

Comments

See what people are discussing